Insurance companies can't reject claims for lack of documents: Irdai

Mumbai. June 11, 2024

The regulator said that the insurer cannot reject claim in full or part if the breach of warranty or condition is not relevant to nature or circumstance of loss

The Insurance Regulatory and Development Authority of India (Irdai) said on Tuesday that no claim shall be rejected by general insurance companies for “want of documents”.

Insurers have been instructed to collect all necessary documents while issuing policies to customers.

Importantly, the regulator has mandated companies to introduce a product with a policy duration of less than a year, with or without provisions for extension or periodic review based on specified criteria, which may include reported or settled claims.

In its master circular on general insurance products, which takes immediate effect, the regulator specified, “The customer may be required to submit only those documents directly related to claim settlement.”

“The necessary documents, such as the claim form, driving licence, permit, fitness certificate, FIR, untraced report, fire brigade report, post-mortem report, books of accounts, stock register, wage register, and repair bills (only in cases where cashless is not available), will be requested at the time of claim settlement,” the circular outlined.

The regulator emphasised that insurers cannot reject a claim wholly or partially if the breach of warranty or condition is irrelevant to the nature or circumstances of the loss. Similarly, delays on the policyholder’s part cannot serve as grounds for rejection unless they result in an increased assessed loss.

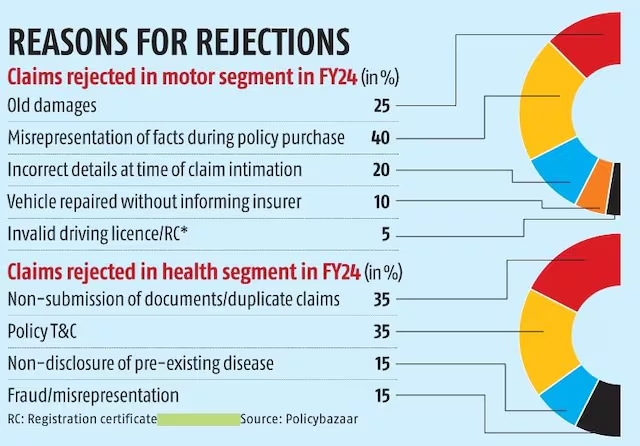

Hari Radhakrishnan, a member of the Insurance Brokers Association of India, noted that this move will likely reduce claim rejections, saying, “Every claim requires specific supporting documents. If the insured cannot provide these at the time of settlement, often due to lack of awareness or inability, claims get rejected citing document insufficiency.”

In cases of partial loss, insurers have been instructed not to burden retail policyholders with salvage disposal. The insurer assumes responsibility for collecting the salvage amount, while the customer receives the claim amount.

Salvage value represents the amount the damaged asset would fetch in the open market, deducted from the claim amount.

To expedite claim settlement, general insurers must assign surveyors through the General Insurance Council’s (GIC’s) technology (tech)-based solution within 24 hours of a claim report. Surveyors are expected to submit their reports to the company within 15 days.

An insurance surveyor and loss assessor, licensed by the regulator, assess losses when an insurance claim is filed.

Upon receipt of the report, the insurer must settle the claim within seven days. Any delays beyond the stipulated timelines would be a violation, subject to penalties.

To enhance transparency in surveyor allocation, the regulator has directed the GIC to develop a technology-based solution for assigning survey work based on area, line of business, qualification, and other relevant factors. This system, to be operational by October 31, 2024, will randomly assign surveyors and notify customers.

Insurers must establish board-approved criteria for monitoring surveyor performance, including turnaround time, accuracy, and report speed, while informing policyholders of claim settlement timelines.

Regarding policy cancellation, Irdai permits retail customers to cancel policies at any time without giving reasons, while insurers can cancel policies on established fraud grounds with a minimum seven-day notice. However, statutory motor third-party liability insurance or legally mandated insurances cannot be canceled except for cases of double insurance or total loss.

Insurers must refund a proportion of the premium for the unexpired policy period if no claims were made and coverage for subsequent policy years has not commenced.

These changes align with the regulator’s shift from rule-based to principle-based regulations, aiming to facilitate business operations, encourage innovation, and adapt to changing market dynamics efficiently.

Insurers are also required to introduce a customer information sheet and establish governance mechanisms to strengthen insurance contract stages, from product development to policy servicing. Pricing should reflect risk exposure, experience, and expenses, ensuring rates are fair and non-discriminatory.

Insurers must incorporate risk management into product design, preventing and mitigating risks, and refrain from unprincipled rate-cutting and improper underwriting practices.

The regulator also recommends offering ‘pay as you drive’ or ‘pay as you go’ options in motor insurance and providing a wider range of add-ons for homeowners, covering various perils, exposures, and lines of business, with options to include or exclude specific covers such as flood, cyclone, earthquake, terrorism, etc.

[The Business Standard]