ITR utility updated: New 'other income' column added under exempt income schedule; here's what it means

Jul 6, 20261

Synopsis

Income Tax Return (ITR) filing for the assessment year 2026-2027 sees a significant update with a new 'Other Income' column under the Exempt Income Schedule. This allows taxpayers to voluntarily disclose non-taxable receipts that don't fit specific categories, like rural agricultural land sales or gifts from relatives. Experts advise this proactive reporting to prevent potential tax notices and mismatches with departmental records, especially for substantial transactions.

If you are salaried, a pensioner, a student, or anyone else who doesn't need to do an income tax audit, make sure to file your income tax return (ITR) by July 31, 2026 for the assessment year 2026-2027. The deadline for filing ITR for the Tax Year 2026-2027 is July 31, 2027.

This year, the ITR filing utility has been updated to factor in a bunch of suggestions by taxpayers and updates from the new Income Tax Act. One such feature relates to exempt income. Usually there is no tax to be paid on exempt income but experts recommend reporting it just in case you face any scrutiny later on, so you can clarify it.

Chartered Accountant Himank Singla mentioned on X that while you didn't need to report the sale of rural agricultural land or gifts from relatives since they aren't considered income, many professionals still included them under the Exempt Income Schedule to avoid unnecessary tax notices. However, this reporting mechanism is now being re-introduced after being taken away.

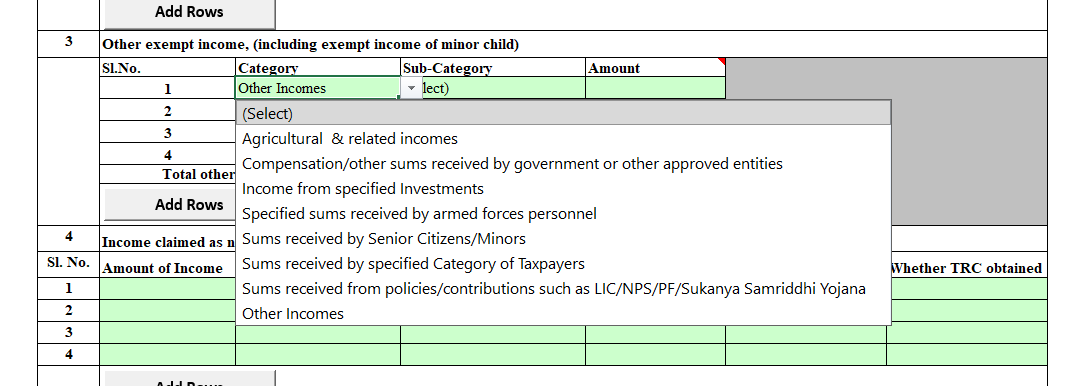

ITR utility

Source: CA Suresh Surana

What it means

Chartered Accountant Suresh Surana told ET Wealth Online that initially, the ITR utility for AY 2026-27 did not provide a clear residual category for reporting "Other Exempt Income" under Schedule EI. This had created practical concerns in cases where taxpayers wanted to voluntarily disclose exempt income which did not fall under the specific categories available in the utility.

Surana says: "However, the updated utility now provides a residual category option by including a column for "Other Income" under exempt income."

According to Surana, this means that where a taxpayer has a receipt which is exempt but does not fit into a specific exempt income category, the taxpayer may now have a route to disclose that income.

Also, receipts like sale consideration from rural agricultural land and gifts received from specified relatives are not required to be added to taxable income.

In the case of sale of rural agricultural land, if the land does not qualify as a "capital asset" under Section 2(14) of the Income-tax Act, 1961, the transfer does not give rise to taxable capital gains.

Surana says: "Therefore, such sale consideration should not be offered to tax as capital gains. Similarly, gifts received from specified relatives are not taxable under section 56(2)(x)."

What should taxpayers do?

Considering the updated ITR utility now provides a residual disclosure field under Schedule EI for "Other exempt income", Surana says taxpayers should consider making a voluntary disclosure of non-taxable receipts.

This approach may be helpful, particularly when the transaction value is significant or the receipt is likely to be reflected in AIS, SFT, bank statements or other information available with the Income Tax Department.

Surana says: "Such disclosure may reduce the possibility of mismatch-based queries or notices and may demonstrate that the taxpayer has considered the transaction while filing the ITR."

[The Economic Times]